Withholding Tax Rates:

Withholding Tax Rates:

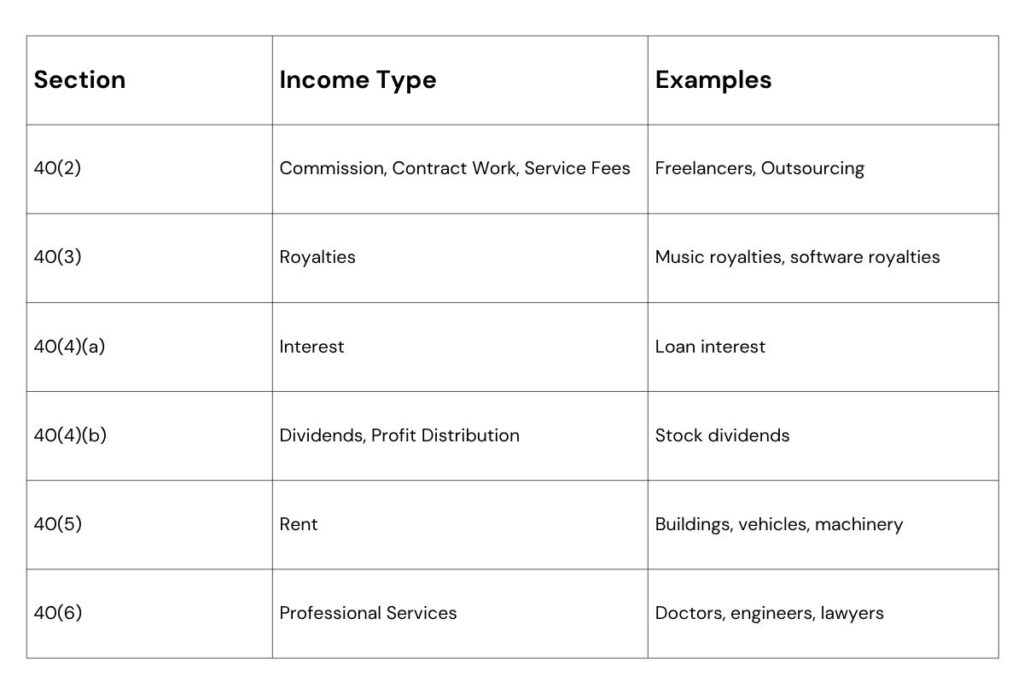

- General payments (Sections 40(2)–(6), excluding dividends): 15%

- Dividends (Section 40(4)(b)): 10%

- Gains from disposal of profits offshore (Section 70 bis): 10%

Filing Deadline:

Submit online by the 15th of the following month. What is Form P.N.D.54?

What is Form P.N.D.54?

It is the withholding tax return form for corporate income tax and gains from disposal of profits (under Sections 70 and 70 bis) paid to foreign juristic persons who do not operate a business in Thailand.

Who must file Form P.N.D.54?

- Payers, which may be individuals, partnerships, companies, or juristic persons in Thailand

- When making payments classified as assessable income under Sections 40(2) to 40(6) to foreign juristic persons

Examples include fees, commissions, royalties, interest, rent, or professional service fees.